How to Incorporate High Implied Volatility Stocks into Conservative Covered Call Portfolios – February 9th, 2026

Elite-performing securities with high implied volatility represent good news/bad news scenarios for our covered call portfolios. The good news is the high premium yields received. The bad news is the risk to the downside. This article will analyze an approach to using these stocks and ETFs to generate significant returns while still aligning with our capital preservation goal. To accomplish this, we will identify the implied volatility (IV) and then use Delta and calculations to guide us to appropriate low-risk, high-yield potential trades.

Real-life example with Global X Uranium ETF (NYSE: URA)

On 9/22/2025, URA, an exchange-traded fund, was trading at $49.43. Since this is a high IV ETF, we can opt for ITM covered calls where the intrinsic-value component of the premium will create greater protection to the downside. We also want to confirm that these defensive trades will still generate adequate returns to justify the trades.

URA 1-month option chain to access the at-the-money IV

- The $49.00 near-the-money strike shows an IV of 47%

- This was triple that of the S&P 500

- To use this elite-performer, while taking a defensive posture, we turn to in-the-money (ITM) call strikes

- Will these ITM strikes provide protection to the downside while still offering significant time-value profit returns?

The significance of Delta when selecting defensive ITM strikes

One of the three definitions of Delta is the approximate probability of the option strike expiring ITM. We want the option to expire ITM to maximize our trade results. For example, if a stock is trading at $50.00 and we sell a $40.00 ITM call for $11.00, we will maximize our return as long as share value remains above the $40.00 strike. Delta will quantify that expectation. Therefore, when we analyze an option chain, we want a high Delta strike that also returns our pre-stated initial time-value goal range. This range is lower than for traditional (more aggressive) covered call writing.

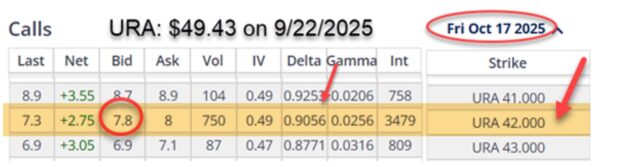

URA 1-month option chain for high Delta strikes

- The $42.00 deep ITM call strike shows a delta of 90.6%

- This means there is approximately a 90.6% probability that URA will expire ITM, which is what we want

- The risk of expiring OTM and subject to losses is 9.4%

- If this risk factor aligns with our personal risk-tolerance, we turn to the BCI Trade Management Calculator (TMC) to see if we can generate our pre-stated initial time-value return goal range

- Let’s feed that $7.80 bid price (red circle) into our TMC

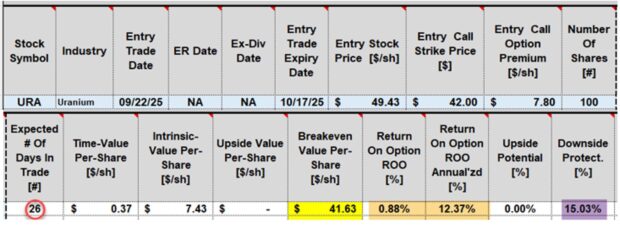

Initial trade deep ITM covered call calculations

- Red circle: This is a 26-day trade if taken through contract expiration

- The breakeven price (yellow cell) is $41.63 (from $49.43)

- The 26-day return is 0.88%, 12.37% annualized (brown cells)

- The downside protection of that time-value profit is 15.03% (purple cell)

- Is a > 12% annualized return with > 15% protection to the downside a trade you’d make? For most, yes; for some, no.

Discussion

Mastering options will allow us to convert high-volatility securities into low-risk option trades. Risk can be quantified using Delta and option chains along with the BCI TMC will provide initial calculations to complete the analysis.

Author: Alan Ellman