How to Calculate and Archive Results for a Rolling-Out-And-Up Covered Call Trade – November 24, 2025

When a covered call trade is expiring in-the-money (ITM), we may have an opportunity to retain the underlying shares by rolling-out or rolling-out-and-up. The latter is a more aggressive form of rolling. This article will scrutinize a series of real-life trades, shared by Bob, a BCI Premium Member, to demonstrate how to calculate and determine initial and final returns.

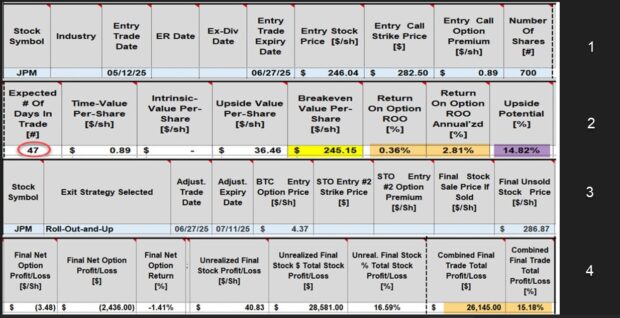

Bob’s trades with JPMorgan Chase (NYSE: JPM)

- 5/12/2025: Buy 700 x JPM at $246.04

- 5/12/2025: STO 7 x 6/27/2025 $282.50 calls at $0.89

- 6/27/2025 (expiration Friday): BTC 7 x 6/27/2025 $282.50 calls at $4.37

- 6/27/2025: JPM trading at $286.87

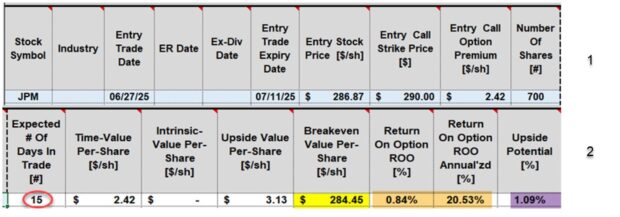

- 6/27/2025: STO 7 x 7/11/2025 $290.00 calls at $2.42 (rolling-out-and-up from the $282.50 strike)

JPM final calculations for the 6/27/2025 expiration (BTC aspect of rolling included)

- Section # 1: Initial trade entries in our BCI Trade Management Calculator (TMC)

- Section # 2: Initial trade calculations (0.36%, 2.81% annualized with 14.82% upside potential). The maximum return is 15.18%

- Section # 3: Trade adjustment with the BTC at $4.37 (1st leg of rolling-out-and-up)

- Section # 4: Final trade results after closing the short call shows a net unrealized (shares not sold) return of 15.18%. Typically, there is a loss of a few pennies when closing a deep ITM call as expiration approaches

JPM initial calculations for the 7/11/2025 expiration (STO aspect of rolling included)

- Section # 1: Initial trade entries

- Section # 2: Initial trade calculations (15-day return of 0.84%, 20.53% annualized, with upside potential of an additional 1.09%

***When rolling an option, I prefer to enter the cost-to-close in the original contract calculations and the sell-to-open rolling premiums in the later-dated contracts.

Discussion

When rolling a covered call trade out-and-up, the BTC of the original short call can be applied to the initial trade (my preference) or the rolled expiration. If the BTC debit is included in the later-dated contract, the premium amount entered will be the debit + the credit. In these trades, it would be a premium of -$4.47 + $2.42 = -$2.05. You can see how this would throw off the 20%/10% guideline calculations in our TMC. My preference is to include the BTC debit with the initial contract and the STO credit with the later-dated contract. Although the combined results are the same, the exit strategy buyback price points are easier to calculate. As a matter of fact, if managed this way, the TMC spreadsheet will do these exit strategy calculations accurately for us.

Author: Alan Ellman