Strike Selection After Rolling-Out Our Portfolio Overwriting Trades – November 10, 2025

Portfolio overwriting is a covered call writing-like trading strategy. There are 2 distinctly defined goals: generating cash flow + retention underlying shares. Since deep out-of-the-money (OTM) strikes are used to align with the goal of share retention, our % premium returns are expected to be significantly lower than those of traditional covered call writing. 4% – 15% annualized returns is a reasonable guideline range. When share retention is super-critical, lower annualized returns are appropriate. This does not include share appreciation or dividend income, when applicable.

Despite selecting deep OTM call strikes, there are times when a strike is expiring in-the-money (ITM), and we roll the option to avoid exercise. When the original short call is closed, there is an option debit which impacts the final returns. So, how does that debit impact our decision regarding our strike selection for the later-dated option contracts? Should it have any influence at all on those determinations? This article will analyze a real-life example with NVIDIA Corp. (Nasdaq: NVDA).

NVDA trades from 5/12/2025 – 6/20/2025

- 5/12/2025: Buy 100 x NVDA at $123.00

- 5/12/2025: STO 1 x 6/20/2025 $143.00 call at $1.56

- 6/20/2025: NVDA trading at $143.85, leaving the $143.00 call ITM as the option is approaching expiration at 4 PM ET

- Roll the 6/20/2025 $143.00 call (buy-to-close at $0.88) to the 7/18/2025 $160.00 call (sell-to-open at $0.78). This is known as rolling-out-and-up.

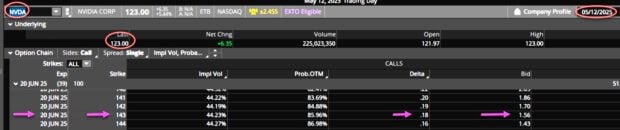

NVDA option-chain on 5/12/2025

- With NVDA trading at $123.00, the 6/20/2025 $143.00 strike has a bid price of $1.56 and a delta of 18% (probability of expiring ITM and subject to exercise)

- This is a reasonable approach to portfolio overwriting. For less risk of exercise, use higher-strike, lower-delta options. When retention of underlying shares is absolutely essential to the strategy goals, deltas ranging from 2% -5% may be more appropriate

Calculations after closing the $143.00 short call on 6/20/2025 (deducting the $0.88 BTC debit from the $1.56 premium)

- Using the BCI Trade Management Calculator (TMC):

- Prior to selecting the next contract strike, the final option return was 0.55%, 5.04% annualized, successful portfolio overwriting result (brown cells)

- This includes the BTC debit of $0.88

- There is also an unrealized gain of 16.26% of share appreciation (purple cell)

- What is the best strike to select for the 7/18/2025 contracts?

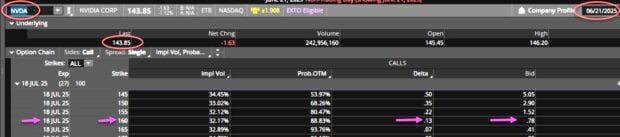

NVDA option-chain on 6/20/2025 for the 7/18/2025 expirations

- We evaluate the risk of exercise by looking at a deep OTM call strike with low Delta

- The 7/18/2025 $160.00 call strike has a Delta (risk factor) of 13% and a bid price of $0.78

- The initial rolled returns are 0.54%, 7.07% annualized

- These are reasonable portfolio overwriting returns with a risk factor of 13%

- If NVDA is trading > $160.00 as expiration approaches, the option can be rolled again

Discussion

When using the strategy of portfolio overwriting, rolling an option plays no role in strike selection for the later-dated contracts. Since share retention is a critical aspect of the strategy, only deep OTM strikes are used based on their associated risk of exercise factors. The more critical share retention is to the strategy, the lower deltas (2% – 5%) should be favored.

Author: Alan Ellman