Buffer ETFs and the Collar Strategy – December 15, 2025

Buffer ETFs have become popular over the past few years. Covered call writers can draw a reasonable analogy between the collar strategy and these buffer securities. This article will highlight the similarities and draw some conclusions.

What is a Buffer ETF?

Also known as a defined outcome ETF, predominantly on indexes, provides investors with a specified amount of downside protection against losses while also capping potential gains. Options are used to achieve specific risk/reward outcomes.

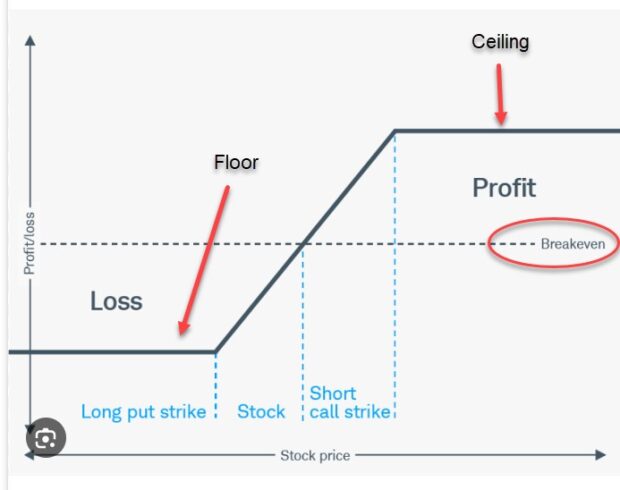

What is the collar strategy?

This is a covered call writing-like strategy where a protective put is added to a covered call writing trade. The 3 legs of the trade are:

- Long stock position

- Short call position (ceiling)

- Long put position (floor)- This establishes a hard floor, whereas as buffer ETFs offer significant but limited protection to the downside

Here is an image of the collar strategy:

Example of a Buffer ETF: FT Vest Laddered Buffer ETF (BATS: BUFR)

- Largest buffer ETF by assets under management

- 10% buffer against losses (the fund absorbs the 1st 10%, but not beyond)

- Caps the upside at 12.7% – 16.9%, depending on when shares are purchased

- Expense ratio (fees) of 0.99%

- Vanguard’s S&P 500 index fund (VFIAX) has an expense ratio of 0.04%, as a comparison

- BUFR must outperform the market by >0.95% achieve greater results than VFIAX

1-year comparison chart between BUFR and VFIAX

- This chart is typical of most timeframes

- Since our covered call strategies, including the collar, generally outperform the overall market, I would expect the collar to outperform the buffer ETFs in the long run

Discussion

The collar strategy and buffer ETFs both offer a ceiling on profits and a floor to the downside. For buffer ETFs, that floor is limited, for the collar, it is a hard floor, ensuring a maximum defined loss. It is reasonable to expect the collar to outperform buffer ETFs in most timeframes.

Author: Alan Ellman