Lowering Cash-Secured Put Breakeven Price Points Means Greater Protection to the Downside with Lower Premium Returns – December 22, 2025

When executing our cash-secured put trades in bear, volatile or uncertain market conditions, it is reasonable to structure our trades with lower breakeven price points. This will come at the expense of lower initial time-value returns. It is imperative that we identify our initial time-value return goal range prior to establishing such trades. What is the minimum acceptable return for the greatest amount of downside protection? In this article, a real-life example with NVIDIA Corp. (Nasdaq: NVDA) will be analyzed.

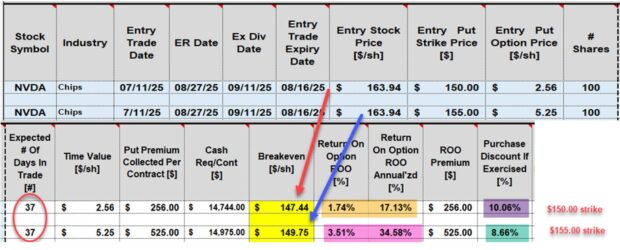

NVDA put option-chain on 7/11/2025 (8/15/2025 expiration)

- The OTM $160.00 put has a bid price of $5.25 (yellow row)

- The much deeper OTM $150.00 put has a bid price of $2.56 (brown row)

NVDA put calculations on 7/11/20265 using the BCI Trade Management Calculator (TMC)

- This is a 37-day trade, if taken through expiration Friday (red oval)

- The $150.00 deep OTM put strike has a breakeven price point of $147.44 (red arrow)

- The $150.00 strike has an initial time-value return of 1.74%, 17.13% annualized (brown cells)

- The $150.00 put offers 10% protection to the BE (purple cell)

- The $160.00 OTM put has a breakeven price point of $149.75 (blue arrow)

- The $160.00 strike has an initial time-value return of 3.51%, 34.58% annualized (pink cells)

- The $160.00 put offers 8.66% protection to the BE (green cell)

Discussion

When establishing defensive cash-secured put trades, monitoring the breakeven price points are instructive. The lower the better as it relates to insurance against share price decline. The lower the breakeven price point, the lower the time-value returns. There’s a tradeoff. We must establish our initial time-value return goal range prior to crafting our trades and then locate the lowest BE price point that meets our pre-stated goals. Once our trades are entered, we immediately prepare for potential exit strategy opportunities.

Author: Alan Ellman