Unlocking the Mystery of Longer-Dated Call Options & Delta – January 19, 2026

Covered call writers (put sellers, too) may analyze Delta stats prior to executing option trades. This article will explore the relationship between Delta and time-to-expiration. Who thinks Delta goes up over time? Who believes it goes down over time? Who thinks something else? Let’s see.

3 Definitions of Delta

- Delta is the amount an option price will change for every $1.00 change in share price

- Delta is the equivalent number of shares represented by the options position

- Delta is the percentage likelihood that, upon expiration, the option will expire in-the-money (ITM) or with intrinsic value

A majority of covered call writers are interested in the likelihood of their options being exercised and the shares sold. Delta provides insight into this concern. A Delta, for example, of 80 (.8 or 80%) suggests an approximate 80% probability of expiring in-the-money (ITM) or with intrinsic-value and, therefore, subject to exercise.

What happens to Delta stats as we go out further in time using the same strike prices?

Real-life example with Apple, Inc. (Nasdaq: AAPL)

On 9/4/2025, AAPL was trading at $238.03. We will check the option-chain data for the 1-month and 6-month $225.00 (ITM) and $250.00 (OTM) strikes, as they relate to the approximate probability of expiring ITM.

AAPL 1-month option chain

- The ITM $225.00 strike has a Delta of 80.1% (lower red oval)

- The OTM $250.00 strike shows a Delta of 24.2% (blue oval)

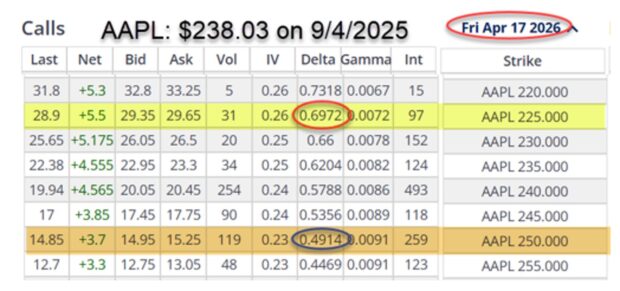

AAPL 6-month option chain

- The ITM $225.00 strike has a Delta of 69.7% (lower red oval)

- The OTM $250.00 strike shows a Delta of 49.1% (blue oval)

Comparing ITM & OTM Deltas

ITM $225.00 strike: As we went out in time, this strike went from a Delta of 80.1% to 69.7%. Why? Well, it started ITM and going out 6 months will give AAPL ample opportunity to move below the ITM strike and therefore, is slightly less likely to expire with intrinsic value.

OTM $250.00 strike: As we went out in time, this strike went from a Delta of 24.2% to 49.1%. Quite a difference. Why? Over a 6-month timeframe, AAPL can certainly move from $238.03 to above the $250.00 strike, rendering the $250.00 strike now ITM, if that occurs. The probability of expiring ITM increases over time.

Discussion

As we use longer-dated options, Delta will slightly decrease for ITM strikes and increase for OTM strikes. If you said, “Delta goes up”, partial credit. If you said, “Delta goes down”, partial credit. If you said, “something else”, partial credit- sorry, you didn’t specify.

Author: Alan Ellman