Can We Use 2 Standard Deviation Implied Volatility When Portfolio Overwriting? – February 23, 2026

Portfolio overwriting is a form of covered call writing where share retention, capital preservation and generation of modest cash flow are specified goals. We are looking to generate an additional option premium income stream while retaining the underlying shares. The risk of exercise and sale of our shares will always be present, but we can craft our trades in such a manner that the risk becomes much less than 1%.

What is standard deviation (SD)?

This is a measure of the range in a data set showing how far, on average, data points move from the data’s mean average.

What is 1 SD as it relates to implied volatility (IV) & stock price movement?

This quantifies the market expectation of a stock’s price movement over 1 year, falling into that range 68% of the time. Let’s say a stock is trading at $100.00 and its at-the-money (ATM) IV is 25%, we expect price movement to fall into the $75.00 – $125.00 range 68% of the time. We can take advantage of SD IV to assist in selecting strike prices based on our strategy goals.

How does 1 SD IV apply to Portfolio Overwriting?

Since we don’t want our shares sold, we select strikes so high that the probability of exercise is extremely low. BCI has developed a calculator (BCI Expected Price Movement Calculator) that has a conversion formula inherent in the spreadsheet that will convert the annual IV to one specific for the contract we are considering and offer a trading range based on 1 SD IV. Since the data will fall outside that range 32% of the time, our concern is only the 16% at the upper end of the range. Bottom line: When using 1 SD IV, the risk of exercise factor is approximately 16% (1/2 32%).

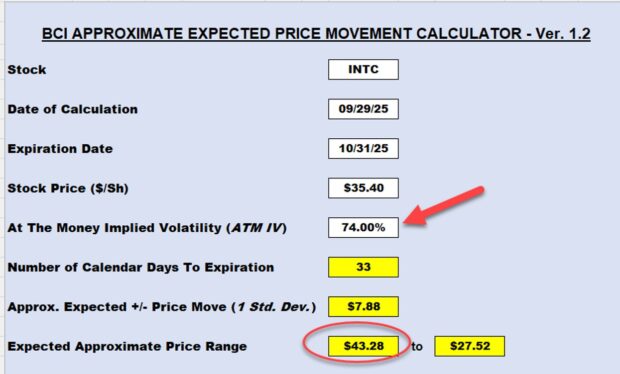

Real-life example with Intel Corp. (Nasdaq: INTC) using the BCI Expected Price Movement Calculator (ATM IV = 74%)

- Data entry in the white cells

- 74% IV is for 1 year; the spreadsheet has a conversion for this 33-day trade

- Based on 1 SD, INTC is expected to move up or down by $7.88 (above red oval)

- We would consider a strike $43.00 or higher for a 16% risk of exercise factor and this does not include our ability to buy back the option prior to contract expiration, making the practical risk <1%

Can we use 2 SDs and how is that calculated?

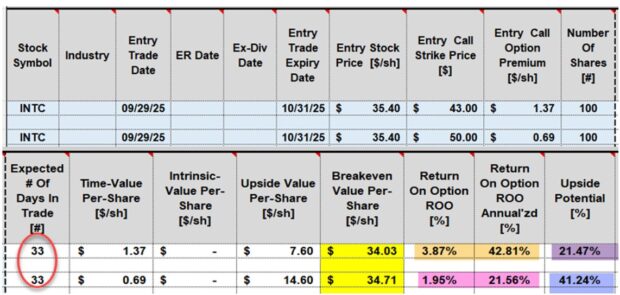

2 SDs is simply double 1 SD. In this case, INTC is expected to move up or down by $15.76 (2x $7.88) 95% of the time. Based on 2 SDs, we would select strikes above $50.00. The risk of exercise is 1/2 5% = 2/1/2%, w/o exit strategies.

Can we make any significant returns using 1- and 2 SDs?

INTC had an extremely high IV at the time I was writing this article. Lower IVs would generate lower returns, but let’s move on with the calculations. The $43.00 strike (1 SD) shows a bid price of $1.37, and the $50.00 strike (2 SDs) has a bid price of $0.69.

1- & 2-SD calculations using the BCI Trade Management Calculator

- 1 SD: The $43.00 OTM strike returns 3.87% in 33 days, 42.81% annualized (brown cells). There is also 21.47% upside potential (purple cell) if INTC moves up to or beyond the $43.00 strike.

- 2 SD: The $50.00 OTM strike returns 1.95% in 33 days, 21.56% annualized (pink cells). There is also 41.24% upside potential (blue cell) if INTC moves up to or beyond the $50.00 strike.

Discussion

2 SD IVs can be used for portfolio overwriting, particularly for high IV options. The approximate risk of exercise is 2.5%. With exit strategies it becomes < 1%.

Author: Alan Ellman