How to Incorporate High Implied Volatility Stocks into Conservative Cash-Secured Put Portfolios – February 16, 2026

In a previous publication, a high implied volatility (IV) ETF, URA was analyzed as how to use it in a defensive manner while still generating significant covered call writing returns. In this article, a real-life cash-secured put trade with Solaris Energy Infrastructure Inc. (NYSE: SEI) will be investigated. Why SEI? After the BCI Weekly Stock Screen & Watch List was published, I looked for the highest IV stock that had adequate option liquidity and no earnings report (ER) concerns. SEI stood out with an enormous IV of 83.7%. Can we generate decent returns and still craft trades with a low risk of exercise?

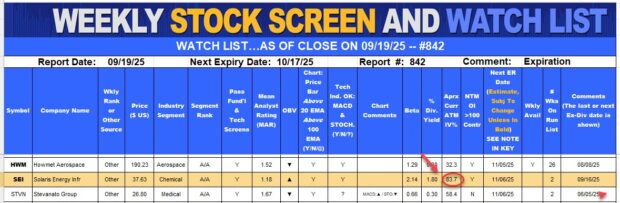

SEI on our Premium Member Stock Report

- Note the IV of 83.7% (circled with red arrow)

Real-life trade with SEI on 9/22/2025

- SEI trading at $37.63

- The 10/17/2025 $25.00 put has a bid price of $0.21

- The $25.00 put shows a Delta of -0.0454 or a 4.5% risk of being subject to exercise at expiration

- SEI next ER date is 11/6/2025

The BCI Trade Management Calculator (TMC)

- Red circle: 26-day trade, if taken through contract expiration

- Yellow cell: Breakeven (BE) price is $24.79 from current market value of $37.63 (red arrow)

- Brown cells: Initial time value return is 0.85%, 11.89% annualized

- Purple cell: Downside protection to BE is a whopping 34.12%

- According to the Delta, the risk of being subject to exercise (without exit strategy intervention) is approximately 4.5%

Discussion

Even ultra-high IV securities can be used in our option portfolios in a low-risk manner, keeping our capital preservation goal in mind. In this case with SEI, the risk of exercise is only 4.5% with the potential of an 11.89% annualized return … singles and doubles, no grand slam homeruns. It is important to always remember that when we craft our trades defensively, rather than traditionally (strikes closer to current market value) we are trading potential returns for protection. However, the returns can still be significant while still benefitting from the downside protection.

Author: Alan Ellman