Comparing the Protection from ITM Covered Calls versus Adding Protective Puts (The Collar Strategy) – March 23, 2026

In bear, volatile and uncertain market environments, covered call writers turn to ITM call strikes and protective puts to create greater protection to the downside. In this article, the pros & cons of each hedging technique will be analyzed using a real-life example with NVIDIA Corp. (Nasdaq: NVDA).

Why consider ITM call strikes in challenging market environments?

ITM calls strikes have intrinsic-value components to them (the amount the strike is lower than current market value). This component of the option premium, along with its time-value component will lower the breakeven price point to a greater extent than ATM or OTM call strikes, which have only time-value premium. This additional (limited) downside protection is paid for by the option-buyer (not us) in the form of intrinsic-value. In return from benefitting from taking this defensive posture, we are eliminating any additional income from share price acceleration.

Why consider protective puts (collars) in challenging market environments?

Adding protective puts to our covered call trades (collars) costs money. We, the option sellers, pay for it. Collar trades should be established with a net option credit which will result in a positive initial return, some upside potential, a small zone for potential losses and then protection all the way down to zero (catastrophic share loss is avoided).

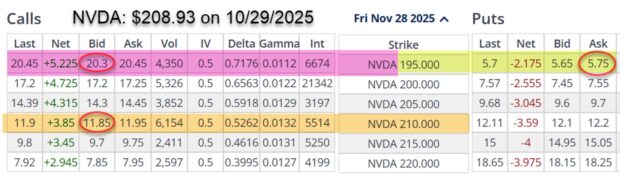

Real-life example with NVDA: 1-month Option chain on 10/29/2025

- For an ITM covered call, we’ll select the $195.00 strike, which has a bid price of $20.30

- For the protective put/ collar trade, we’ll select the OTM $210.00 strike which has a bid price of $11.85, and the $195.00 protective put which has an ask price of $5.75

- The net option credit for the collar is $6.10 ($11.85 – $5.75)

Comparing calculation returns for both approaches using the Trade Management Calculator (TMC)

- THE ITM $195.00 call lowers the BE price to $188.63 (red arrow)

- The collar lowers BE price to $202.83, (blue arrow) but will then also protect against catastrophic share price decline below the $195.00 put strike

- The initial time-value return for the ITM strike is 3.27%, 38.46% annualized (brown cells)

- The initial time-value return for the collar is 2.92%, 34.38% annualized (pink cells) with an additional upside potential of 0.51% (blue cell)

Summarizing returns and protection

- The initial returns are similar so path selection should not be based on initial calculations

- The ITM call offers protection down to $188.63, with risk of share value loss from that point down to zero (of course, we would initiate exit strategy intervention way before zero!)

- The collar offers protection down to $202.83 and then from $195.00 down to zero, leaving a risk range between $202.83 and $195.00

- Given these calculations, each investor can decide which approach aligns best with their personal risk tolerance and strategy goals as both offer significant protection for our covered call trades

Discussion

In bear, volatile and uncertain market conditions, covered call writers can generate significant annualized returns while still crafting their trades to garner substantial protection to the downside. In this article, ITM call strikes and adding protective puts (collars) were analyzed.

Author: Alan Ellman