Using 2 Standard Deviations to Determine the Risk of Exercise of a High Implied Volatility Stock When Covered Call Writing – April 6, 2026

Portfolio overwriting (PO) is a form of covered call writing where, in addition to generating cash flow, we also want to retain the underlying shares. Achieving both goals may become more challenging when employing high implied volatility (IV) securities. In this article, a real-life example with Intel Corp. (Nasdaq: INTC) will be used to analyze such a scenario.

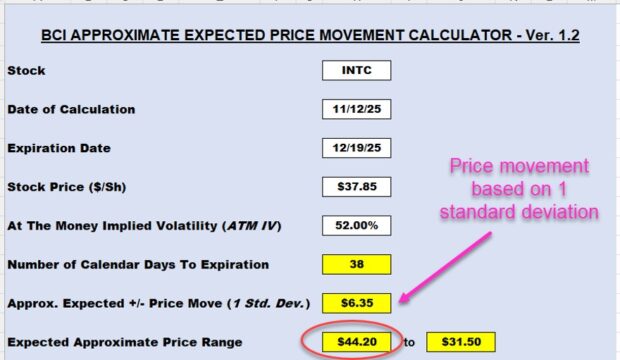

Real-life example with INTC on 11/12/2025

- INTC trading at $37.85

- The near-the-money $38.00 strike shows an IV of 52%

- IV stats are based on 1-standard deviation (1-SD) and 1-year timeframes which need to be converted to the timeframe for the contract in question

- The BCI Expected Price Movement Calculator will do just that

- The BCI Expected Price Movement Calculator will be used to determine an out-of-the-money strike which has a16% risk of being breached (subject to expiring in-the-money and at risk of being exercised or sold)

- We will double the expected price movement to then calculate the 2-SD amount which will provide a strike with only an approximate 2.5% probability of being breached

INTC option chain on 11/12/2025 showing an ATM IV of 52%

BCI Expected Price Movement Calculator to Select PO Strikes Based on 1 Standard Deviation/ 16% risk factor

- If a 16% risk factor is acceptable, share price is expected to move up or down by $6.35, resulting in a strike selection of $44.00.

- A 2 SD strike is calculated by doubling $6.35 to $12.70, leading to a strike of $50.00 ($37.85 + $12.70)

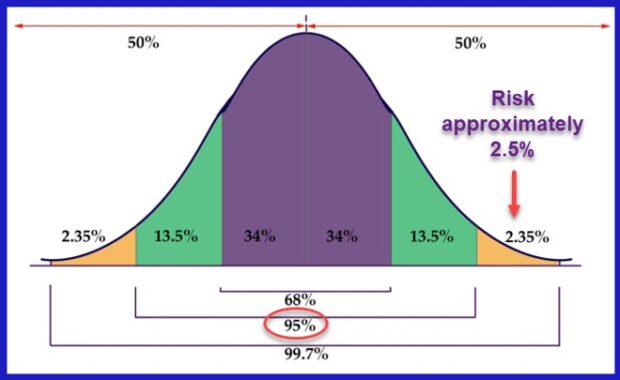

Standard Deviation Bell Curve showing risk factors of 16% (1 SD) and 2.5% (2 SDs)

- 1 SD risk: Green + brown fields on the high end

- 2 SD risk: Brown field only on the high end

Cash flow using this 2 SD approach with this high IV stock

- The $50.00 strike had a premium of $0.46 for the 12/19/2025, 38-day trade.

- This resulted in an initial time-value return of 1.22%, 11.67% annualized.

- Since the $50.00 strike was so deep OTM, an additional 32.10% of upside potential was also available.

Discussion

When using portfolio overwriting with high IV stocks, generating strikes using 2 SDs can result in lower-risk trades which can still generate significant cash flow. Strike selection is always based on both initial time-value return goal range as well as personal risk-tolerance.

Author: Alan Ellman