Laddering Covered Call Strikes Based on Market Assessment and Risk Tolerance – May 4, 2026

What strike should I select for my covered call trades? In-the-money (ITM), out-of-the-money (OTM), how far out, how far in? This apparent dilemma can easily be navigated by identifying our return goals, market assessment and personal risk tolerance. Another important factor is that, when selling multiple contracts, we can use different strikes, a process I refer to as laddering strikes. I borrowed this term from the bond market.

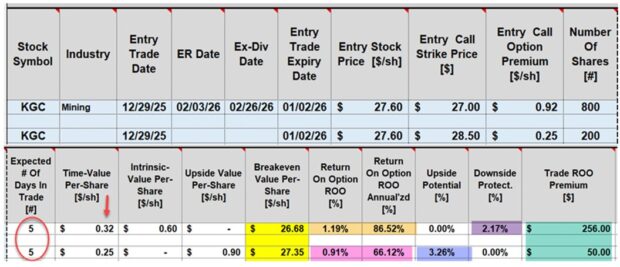

A Real-Life Example with Kinross Gold Corp. (NYSE: KGC) on 12/29/2025 (5-day, holiday-shortened trade)

- 12/29/2025: Buy 1000 x KGC at $27.60

- 12/29/2025: STO 8 x 1/2/2026 $27.00 (TM) calls at $0.92

- 12/29/2025: STO 2 x 1/2/2026 $28.50 (OTM) calls at $0.25

What are these strike selections telling us?

Of the 10 contracts sold, 8 were ITM, a defensive approach; 2 were OTM, a more aggressive approach. Overall, I was leaning defensively, with a cautious overall market assessment, which aligned with my personal risk tolerance at the time of these trades.

What about option premium return goals?

I, typically, target 2% – 4% per month and 1/2% – 1% per week. In these trades, I was at the high end of these ranges.

Initial Covered Call Trade Calculations: BCI Trade Management Calculator (TMC)

- Brown cells: The ITM strikes generated initial returns of 1.19%, 86.52%, with 2.17% downside protection of that time-value profit (purple cell)

- Pink cells: The OTM strike generated 0.91%, 66.12% annualized, with 3.26% of upside potential (blue cell)

- Green cells: A total of $306.00 in time-value premium was generated into my brokerage account

Post expiration results

- KGC closed at $28.30, leaving the $27.00 call expiring ITM and 800 shares were sold at $27.00

- The $28.50 strike expired slightly OTM, so 200 shares were retained

- The initial cash outlay for 1000 shares was $27,600.00

- The realized loss on the sales of 800 shares (ITM strike) was $480.00

- The unrealized gain on 200 shares is $140.00

- Net return on the stock side: -$340.00

- Net realized option premiums: $736.00 + $50.00 = $786.00

- Net realized/unrealized return is +$446.00 = 1.61%, 84% annualized (52 periods)

Discussion

- Significant returns can be generated with 5-day covered call trades even during holiday-shortened weeks

- Option trades can be crafted to align with all market environments and personal risk tolerance

- In the case of KGC, significant 5-day returns were initially captured and realized

- These are low risk, not no risk trades