Using Options to Convert a 9.5% Annualized Loss to a 25.3% Annualized Gain – May 18, 2026

Covered call writing & selling cash-secured puts lower our cost-basis and generate cash flow. These are low-risk (not no-risk) option selling strategies. In this article, a 12-day real-life (from 1 of my portfolios) series of trades will be analyzed with NVIDIA Corp. (Nasdaq: NVDA), where share price declined slightly, but a nice 12-day return was realized, by implementing covered call writing.

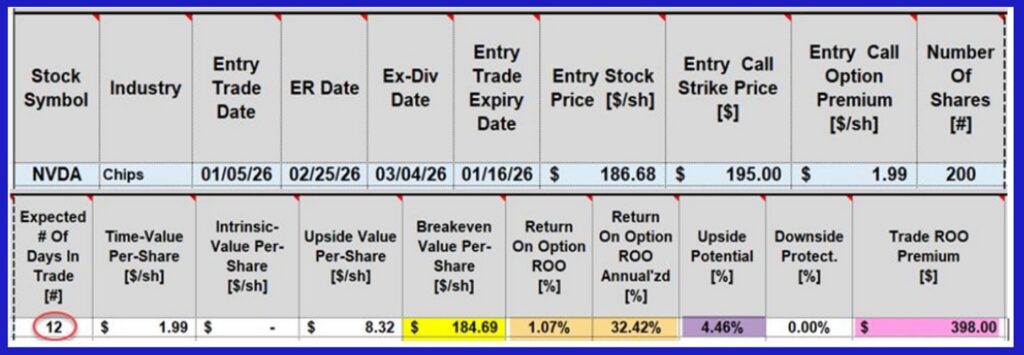

Real-life covered call trades with NVDA

- 1/5/2026: 200 x NVDA purchased at $186.68

- 1/5/2026: STO 2 x 1/16/2026 $195.00 calls at $1.99/share ($398.00 total)

- 1/5/2026: Enter BTC/GTC limit order at $0.20 (10% guideline to protect against share price decline)

- 1/14/2026: The 10% threshold was breached, and the option was rolled down to the $188.00 strike, netting an additional $28.00 in premium

- 1/16/2026 (expiration Friday): NVDA closed at $186.10, leaving the $188.00 strike expiring OTM and expiring worthless (no exercise)

NVDA initial calculations with the BCI Trade Management Calculator (TMC)

- Brown cells: 1.07%, 12-day return, 32.42% annualized

- Purple cell: 4.46% upside potential, if NVDA moves up to, or beyond the $195.00 strike

- Pink cell: $398.00 in premium collected

Rolling-down after breach of 10% guideline (broker confirmation)

Trade Status as of 1/16/2026 After 4 PM ET

- NVDA closed at $186.10, down $0.58 from trade inception (unrealized loss of $116.00)

- The $188.00 strike expires worthless and OTM

- Total option credit: $398.00 + $28.00 = $426.00

- Unrealized share loss: $116.00

- Net realized/unrealized credit = $310.00 ($426.00 – $116.00)

- 12-day return: $310.00/$37,336.00 = 25.3% annualized

- Without options, an annualized loss of 9.5%

Discussion

- Significant initial returns can be generated with 12-day covered call trades

- Option trades can be crafted to align with all market environments and personal risk tolerance

- In the case of NVDA, a significant 12-day unrealized (shares not sold) return was generated despite share value declining

- These are low-risk, not no-risk trades

Author: Alan Ellman