How to Establish a Bear Market Cash-Secured Put Trade- June 1st, 2026

When we sell cash-secured puts, we are contractually obligated to buy shares at the strike price by the expiration date, should the option buyer decide to exercise that option. In the BCI methodology, we predominantly favor out-of-the-money (OTM) put strikes, agreeing to buy the shares at a lower price than current market value.

In bear market environments, we may favor deep OTM put strikes to enjoy the benefit of greater protection to the downside in return for lower option premiums. In this article, we will use one of the option Greeks, delta, to determine strike selection in these situations.

What is delta?

One of the 3 definitions of delta is the approximate probability of a strike expiring in-the-money (ITM) or with intrinsic-value. When this occurs, the option will (almost always) be exercised and shares will be put to the option-seller at the strike price (assuming no exit strategy integration). Typically (but, not always), put sellers want to avoid buying the shares, so delta will measure and quantify that risk. As we go deeper and deeper OTM (strikes much lower than current market value), the risk of exercise becomes less and less as do the option premiums. We must find a balance between risk and returns when establishing our trades.

Real-life example with Solaris Energy Infrastructure Inc. (NYSE: SEI)

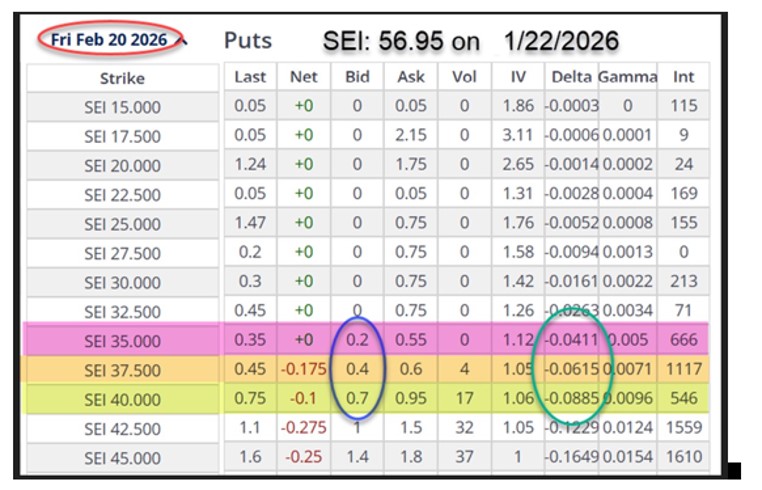

On 1/22/2026, SEI was trading at $56.95. Let’s review the put option chain and look for strikes with deltas < 10%. Note that deltas for puts show a minus (-) sign because put value is inversely related to share price movement.

SEI option chain on 1/22/2026 (SEI: $56.95)

- Red oval: Expiration date is 2/20/2026

- Pink row: $35.00 strike, delta = 4%, bid price = $0.20

- Brown row: $37.50 strike, delta = 6%, bid price = $0.40

- Yellow row: $40.00 strike, delta = 9%, bid price = $0.70

- Note that the lower the risk of exercise (delta), the lower the premium returns

- Let’s calculate the % returns using the BCI Trade Management Calculator (TMC), so we can weigh the risk against the returns

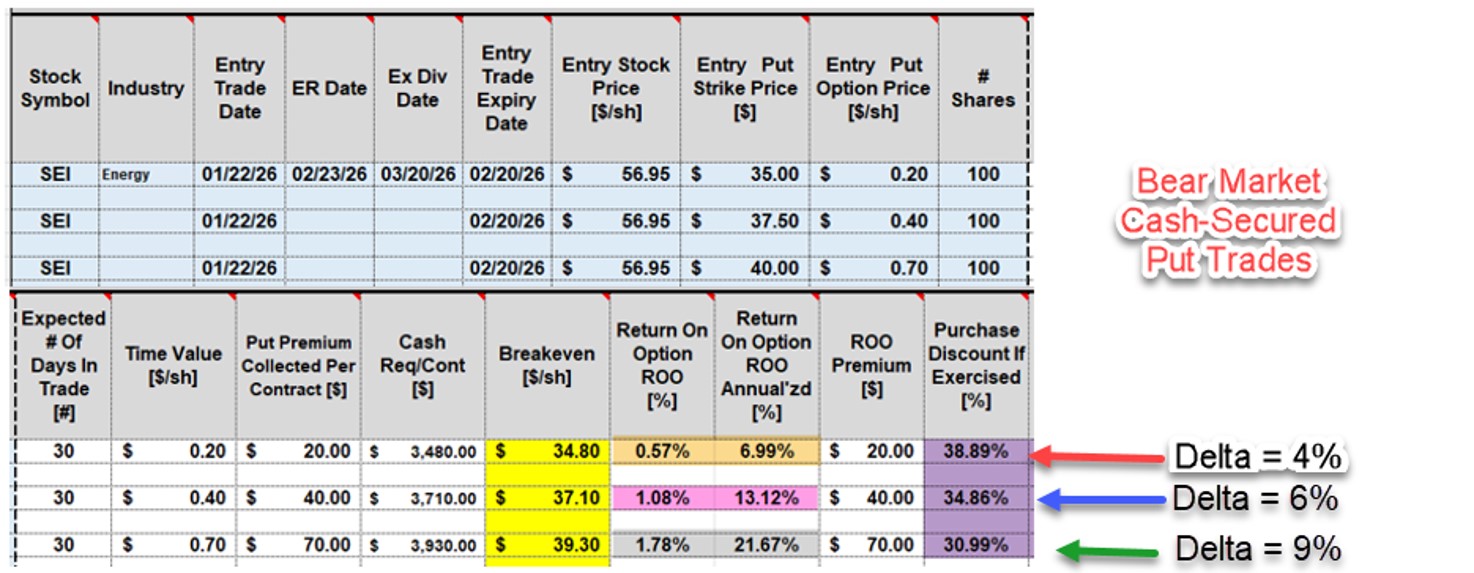

SEI Initial put calculations for the 3 deep OTM strikes

- Red arrow: The $35.00 strike has a delta of 4% and an annualized return of 6.99% (brown cells)

- Blue arrow: The $37.50 strike has a delta of 6% and an annualized return of 13.12% (pink cells)

- Green arrow: The $40.00 strike has a delta of 9% and an annualized return of 21.67% (gray cells)

- The % purchase discount if shares are assigned as a result of exercise (share price moves below the deep OTM strike) ranges from 30.99% to 38.89% (purple cells)

Discussion

In bear markets, we may favor deep OTM put strikes to create greater protection to the downside. Delta is a useful metric that can be implemented to quantify the risk of exercise of the available strikes. We balance risk of exercise with premium returns to guide us to the most appropriate put strikes.