Setting Up a Bitcoin Collar Trade Using the BCI Collar Calculator – June 8, 2026

The most well-known form of cryptocurrency is Bitcoin. I am frequently asked about the use of crypto with our covered call and cash-secured put trades. In this article, a 29-day collar trade s analyzed, using Bitcoin, to construct a defensive, modest-return trade. A real-life example with iShares Bitcoin Trust (Nasdaq: IBIT) is presented.

What is IBIT?

This is an exchange-traded fund (ETF). The shares are intended to constitute a simple means of making an investment similar to an investment in bitcoin rather than by acquiring, holding and trading bitcoin directly on a peer-to-peer or other basis or via a digital asset exchange. Since the implied volatility of this security is robust, there is flexibility that allows us to craft low-risk (not no-risk) trades that still offer significant initial time-value returns.

What is a collar trade?

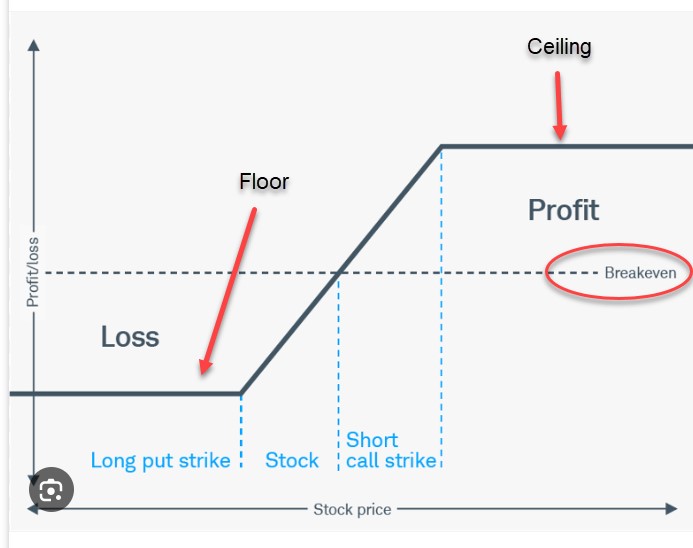

This is a covered call writing-like strategy where a protective put is added to a covered call writing trade. The 3 legs of the trade are:

- Long stock position

- Short call position (ceiling)

- Long put position (floor)- This establishes a hard floor

Here is an image of the collar strategy:

Real-life collar trade with IBIT

- 1/23/2026: 500 x IBIT purchased at $50.55

- 1/23/2026: STO 5 x 2/20/2026 $52.00 calls at $1.65 (ceiling)

- 1/23/2026: BTO 5 x 2/20/2026 $48.00 puts at $1.08 (floor)

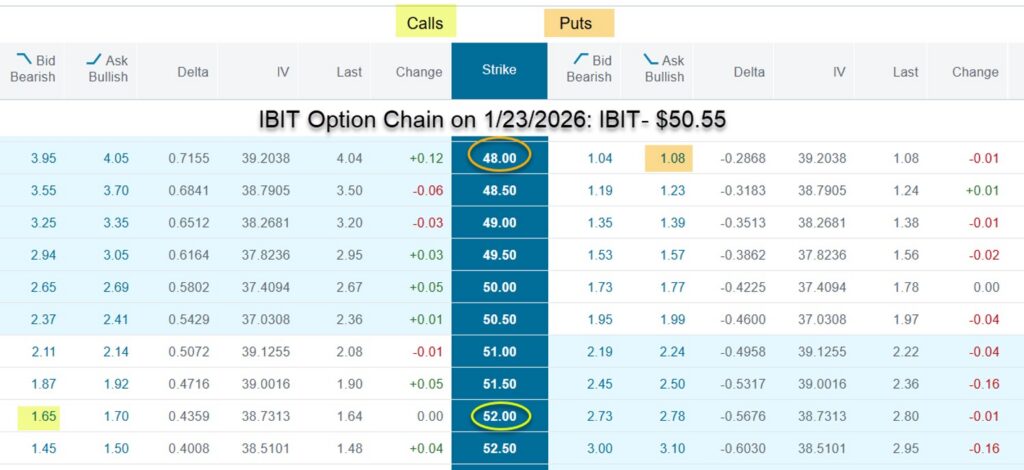

IBIT call & put option chains for this collar trade

- The $52.00 call strike showed a bid price of $1.65 (yellow oval & cell)

- The $48.00 put strike showed an ask price of $1.08 (brown oval & cell)

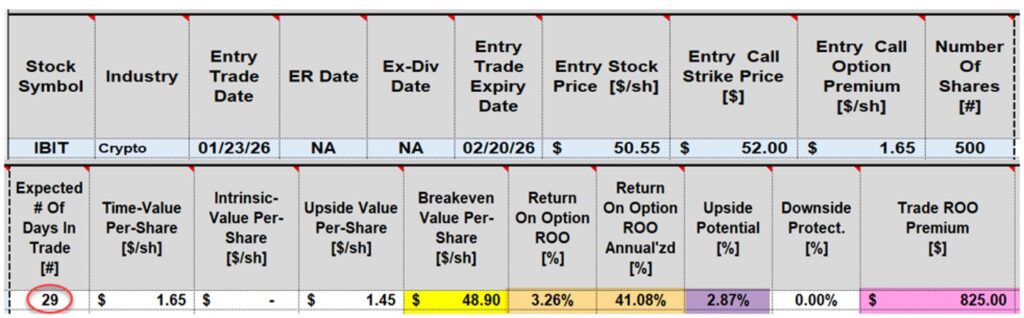

Calculations without the protective put (covered call aspect)

- The BCI Trade Management Calculator (TMC) is used for these calculations

- This is a traditional 29-day covered call trade (red circle)

- The breakeven price point is $48.90 (yellow cell)

- The initial premium returns are 3.26%, 41.08% annualized (brown cells)

- There is additional upside share appreciation potential of 2.87% (purple cell)

- Total cash collected from the sale of the 5 call contracts is $825.00 (pink cell)

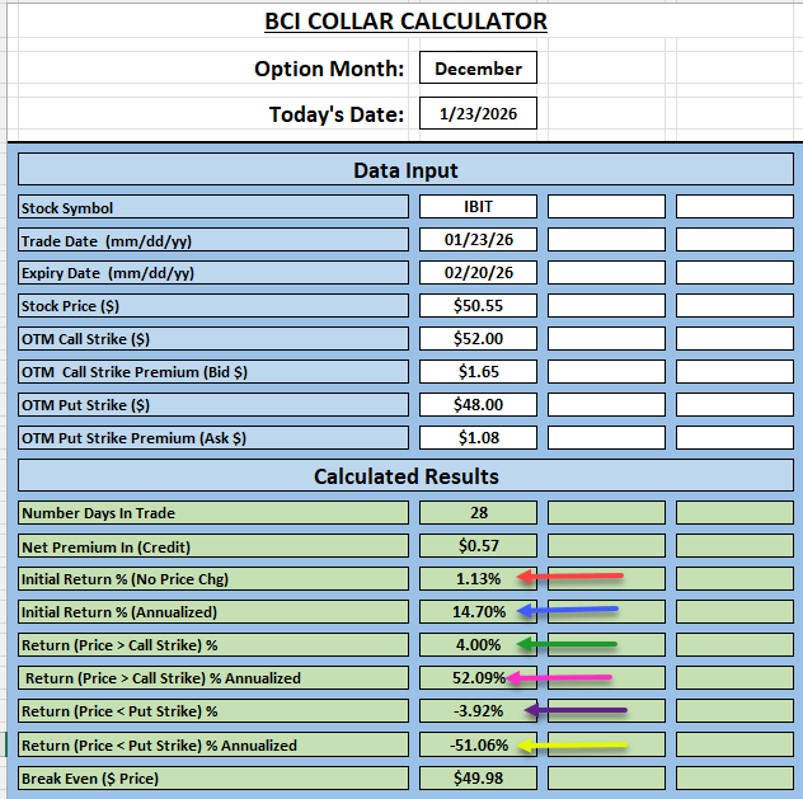

Calculations using the BCI Collar Calculator (adding the protective put)

- This is actually a 29-day trade when including the day of trade entry

- The net option credit is $0.57 ($1.65 – $1.08)

- Red arrow: The initial return on the net option credit is 1.13%

- Blue arrow: The annualized return on the collar trade is 14.70%

- Green arrow: If the share price moves above the call strike by expiration, a 4% return is realized (maximum return)

- Pink arrow: The max return annualized to 52.09%

- Purple arrow: If share price moves below the put strike, there is a loss of 3.92% (max loss)

- Yellow arrow: The max loss annualizes to 51.06%

Can we calculate collar trades using the BCI Trade Management Calculator?

Yes, here’s how: When entering the call option premium in the spreadsheet, enter a net credit amount. In this trade it is $0.57 ($1.65 – $1.08).

Author: Alan Ellman